Understanding Your Financial Advisor’s Credentials

by Gabriel Lewit

When it comes to making important financial decisions, it’s crucial to have all the information you can get. That’s why understanding your financial advisor’s credentials is so important. By knowing what each credential means, you can be sure that your advisor has the experience and expertise necessary to help you reach your financial goals.

experience and expertise necessary to help you reach your financial goals.

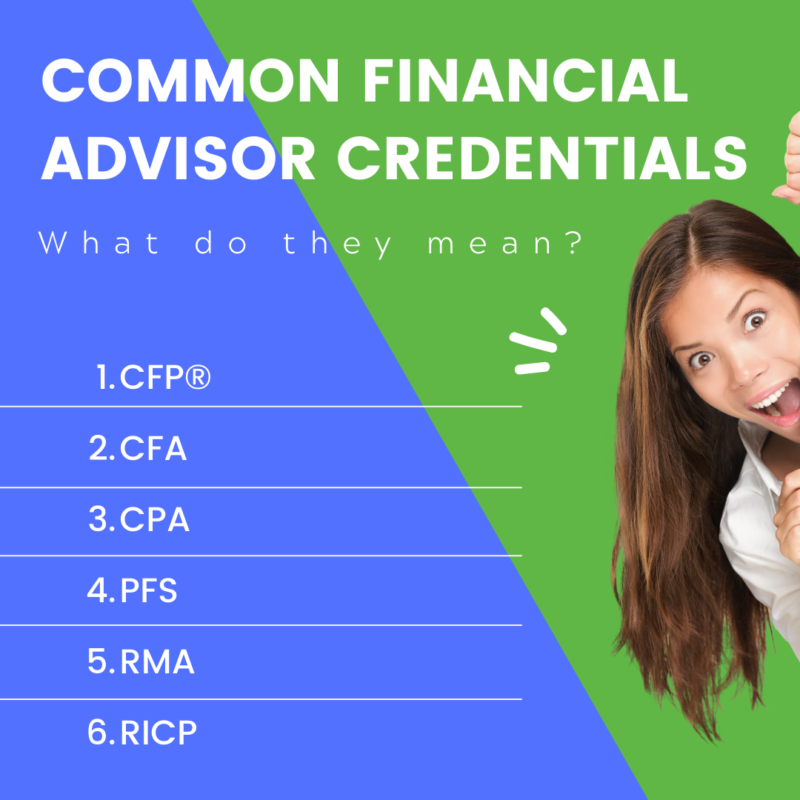

Let’s take a closer look at some of the most common financial advisor credentials, such as:

- CFP®

- CFA

- CPA

- PFS

- RMA

- RICP®

What financial support are you needing currently? A financial advisor in Buffalo Grove, IL can be a life-changer.

What do the letters after your advisor’s name mean and what do they signify about their experience and training?

When people feel the need to hire a financial advisor, they usually start by looking at many options that have confusing credentials behind their names. These defined designations will help you understand what they mean as you proceed in your research.

(CFP®) CERTIFIED FINANCIAL PLANNER™

This kind of professional must live up to the Certified Financial Planner Board of Standards, Inc. The four parts of this kind of professional’s initial certification cover examination, education, experience, and ethics. A CFP® needs coursework in financial planning and a minimum of a bachelor’s degree.

A CFP® can help you manage your finances and get you set up for financial success. This usually involves comprehensive financial planning, investment planning, retirement planning, insurance planning, education planning, estate planning, and tax planning. This individual should be able to adjust your financial plan as you make adjustments to your goals and as life unfolds.

(CFA) Chartered Financial Analyst

The internationally recognized CFA Institute is the issuing body of the reputable Chartered Financial Analyst investing credential. Rigorous experience, education, and examinations are required to earn this title. They too need at least a bachelor’s or have equivalent work experience and education. This kind of professional must maintain professional experience in an investment related field for at least four years.

Because adhering to certain ethical guidelines is required, it’s likely you will receive a high level of investment counsel. They are especially important in portfolio management and investment research.

(CPA) Certified Public Accountant

This designation provides licensed accounting advice. Their licenses are provided by the Board of Accountancy per state and resources to obtain the license are provided by the American Institute of Certified Public Accountants (AICPA). This professional must meet education, work, and examination requirements, hold a bachelor’s in accounting, business administration, or finance, and complete 150 hours of education.

A CPA must also have public accounting experience for two or more years, plus pass the Uniform CPA Exam. They tend to have various positions in corporate/public accounting or have performed the role of chief financial officer (CFO). They can also serve as auditors, business advisers, decision-makers, tax consultants, and accounting consultants.

CPAs tend to be experts in:

- Tax and financial planning

- Assurance services

- Forensic accounting

- Information technology

- International accounting

- Environmental accounting

(PFS) A Personal Financial Specialist

This is a certification for the aforementioned CPA, which allows them to offer financial planning and wealth management. The American Institute of Certified Public Accountants established this designation, with the prerequisite of being a CPA. Per the AICPA, a certification of PFS represents “a powerful combination of extensive tax expertise and comprehensive knowledge of financial planning.”

Areas of study include:

- Retirement planning

- Estate planning

- Investing

- Insurance planning

- Personal financial planning

- Charitable giving

- Fundamental financial planning concepts

- Professional responsibilities, legislative, and regulatory compliance

- Risk management planning

- Employee and business owner planning

- Elder and chronic illness planning

- Educational planning

- Special situations such as divorce

(RMA) Retirement Management Advisor

This financial professional is certified to craft custom retirement plans per client. The RMA designation delineates professionals who have taken additional training in retirement planning. Professionals who most often pursue an RMA certification are:

- Financial planners

- Retirement specialists

- Wealth managers

- Professionals who oversee family offices

- Investment consultants and advisors

- Trust professionals

- Tax professionals

- Estate planning professionals

This professional will focus on accumulating wealth while working with you to create personalized retirement income plans to mitigate risk. A safety-first approach is commonly used beyond wealth building and retirement planning. Their areas of study include:

- Managing household balance sheets

- Asset allocation and risk management

- Retirement phases

- Advisory styles

- Life-cycle financial planning

- Household cash flow planning

- Long-term planning, including Social Security, Medicare, and long-term care needs

- Tax planning

- Retirement withdrawal strategies and policy statements

- Income annuities

- Investment product selection

- Monitoring of financial plans

RICP® Retirement Income Certified Professional

This professional is qualified to assist with planning and carrying out retirement strategies. An RICP can delve deeper than a CFP® into specific areas of retirement income planning and address how retirees can utilize their savings in strategic, smart ways to act on their retirement. A major part of this is how they will be cared for if they can no longer take care of themselves.

Their most common function is to advise near-retirees and retirees on the best ways to use the assets they’ve accumulated for retirement. An RICP can help you make sure you won’t run out of money and live comfortably within a realistic budget.

The Takeaway

So, what should you look for when vetting a financial advisor? In order to make sure that your advisor has your best interests at heart and is not just trying to make a quick buck off of you, make sure that anyone you choose to work with is a fiduciary. This will ensure no conflicts of interest, and that your goals and achievements are on the forefront.

Know that registered advisors must adhere to a code of ethics from the Financial Industry Regulatory Authority (FINRA) and maintain ongoing education requirements. Beyond that, it’s important to understand a financial professional’s experience and investment philosophy.

Do they primarily focus on stocks, bonds, or managed accounts?

What kind of returns have they historically achieved for their clients?

What are their fees and what am I paying for?

Even if an advisor has all the right credentials, you don’t want to be overpaying for their services.

Schedule a meeting with the SGL team!

You have a whole team waiting here to assist you and your family. Call us today.